As subject matter experts, we provide only objective information. We design every article to provide you with deeply-researched, factual, useful information so that you can make informed home electrification and financial decisions.

There’s a reason why more than 2.5 million homeowners have installed solar systems in their homes in the U.S. It’s a smart investment that will increase your home’s value and save you tens of thousands of dollars in electricity costs.

Solar panel systems typically last for 25 years or more, and offset most or all of your monthly electricity bill. Those savings add up quickly: if you pay $150 per month for electricity today, you’ll spend over $65,000 on electricity in the next 25 years. By investing in solar, you can avoid most or all of that future spending on electricity. As with any home improvement or upgrade project, before you install solar panels, it’s important to consider all of the financing options available to you and determine which one best suits your needs.

Electricity Spending | 10 Year Cost | 15 Year Cost | 20 Year Cost | 25 Year Cost |

|---|---|---|---|---|

| $50 monthly bill | $6,900 | $11,200 | $16,100 | $21,900 |

| $100 monthly bill | $13,800 | $22,300 | $32,200 | $43,800 |

| $150 monthly bill | $20,600 | $33,500 | $48,400 | $65,600 |

| $200 monthly bill | $27,500 | $44,600 | $64,500 | $87,500 |

| $250 monthly bill | $34,400 | $55,800 | $80,600 | $109,400 |

Solar financing options

There are three main ways to pay for your home solar system: an upfront cash payment, a solar loan, or through a lease or power purchase agreement (PPA).

If you can’t afford to pay for your system out-of-pocket, solar financing allows homeowners to use products like loans and leases to finance the purchase of a solar system by spreading out the cost over time. A typical solar panel system costs around $25,000 on EnergySage’s marketplace, not including installation.

The two most cost-efficient ways to pay for your solar system are through a cash purchase or a solar loan.

Generally speaking, these two options are the best way to go solar because you either own your own system right away or by the end of your loan. With a cash purchase, you buy your system for its full cost upfront and have no payments moving forward. If you choose a solar loan, it’s similar to financing a car or paying off your mortgage — you’ll be required to make fixed monthly payments over your loan term, which is usually anywhere from five to 25 years.

The third option for financing a new solar system is to enter into a lease or power purchase agreement (PPA). These options aren’t necessarily a smart financial choice because despite paying tens of thousands of dollars, you still won’t own your solar system by the end of the agreement. For example, if you lease a solar panel system for $100 a month for 20 years, you will have spent $24,000 on solar power over two decades, but at the end of the lease you won’t own the system despite spending almost the same amount of money as if you had purchased them.

Cash purchase

Paying for your solar panel system with cash is the best way to maximize your savings from solar. You won’t pay any additional interest like you will with a solar lease, and your electricity costs are taken care of for the next 25 years. You shouldn’t have to pay an electric bill again – or if you do, a very small one. Owning your system outright will insulate you from future electricity rate increases, and you’re eligible to receive all the financial incentives and rebates available to homeowners for going solar.

The main drawback of a cash purchase is that it’s expensive. If you want to buy your system in cash, you’ll need to have enough capital available to pay for the system upfront, which can typically set you back between $20,000 to $30,000, not including installation.

Solar loans

The other primary way to finance a solar panel system so that you own it is with a solar loan.

Solar loans are a good financing option for solar power systems if you can’t afford an upfront payment because they allow you to go solar with no down payment. Although you’ll still own your solar panel system by the end of your loan, the downside is that you’ll have to pay interest on the money you borrow, making a loan a more expensive choice than paying for your home solar system out of pocket. As with any loan, the better your credit, the better the interest rates available to you, and the lower your total costs will be over time.

There are two main types of solar loans, unsecured and secured loans. An unsecured loan doesn’t require any collateral for approval so it will usually have a higher interest rate than a secured loan. A secured loan will tend to have a lower interest rate because it requires you to put up your home as collateral, which is a risky option because if you can’t make your solar loan payments for any reason, your lender can foreclose on your house. Taking out a personal loan or a home equity loan to finance your solar system are other types of financing worth considering, but they have drawbacks like even higher interest rates or require you to put your home up as collateral, too.

Regardless of loan type, you only want to take out a loan for the amount you need and no more so you pay as little interest as possible. As with any financial product, it’s important to pay close attention to the terms and conditions of any loan you’re considering. If you don’t read the fine print, you can end up on the hook for additional fees.

If you’re interested in taking out a solar loan, you can check out some of EnergySage’s available financing partners like GreenBiz Financial and LightStream using our Marketplace.

Solar leases and PPAs

Though they’ve declined in popularity in recent years due to their lack of financial upside, solar leases and power purchase agreements (PPAs) played a major role in the solar industry’s growth in its infancy. Solar leases and PPAs work similarly, which is why they’re often lumped together: they’re both a type of third-party ownership (TPO) where a company installs solar panels on your property and then sells you the electricity produced by the solar panels at a predetermined rate.

With a lease or PPA, you typically lock in a set rate for electricity. That rate should be around 10% to 30% below the rate you currently pay for electricity, according to the U.S. Department of Energy. Leases and PPAs almost always include an annual rate increase, also known as an escalator, which means that each year you pay a higher rate for your solar energy than you did the year before. However, in recent years, the trend has been for leases and PPAs to lock in a specific rate for the full length of the contract. What’s more, with a lease or PPA, the third-party owner is responsible for monitoring the system and any maintenance on it, which can be a positive or a negative depending on how reliable your leasing company is.

Because you don’t own the solar panel system in a lease or PPA setup, you won’t be eligible to receive any of the financial incentives and rebates associated with solar; rather, the company that owns the system will be. Additionally, while homes with solar typically sell for 3-4% more than homes without solar, that’s not necessarily the case with a lease or PPA because the new homeowner may not want to take over the additional monthly payment for your solar lease.

Note: third-party ownership isn’t available in every state. You can look at DSIRE’s map of states that allow solar leases and PPAs to see if they’re available where you live.

Tax benefits and rebates for solar panels

Rebates and incentives are available to help you pay for solar panels, and they can go a long way towards offsetting your costs. The most valuable incentive tends to be the federal solar tax credit, also known as the investment tax credit (ITC), which credits you 30% of the cost of your solar panel system from your federal income tax. The ITC is set to stay at 30% until 2033, after which it’s set to drop to 26%. There’s no cap on the value of the eligible system – you can deduct 30% of the total cost of your system no matter how much you paid for it.

State and local incentives are also available depending on where you live. New York, Rhode Island, Iowa, Connecticut, and Maryland are some of the friendliest states for solar tax incentives.

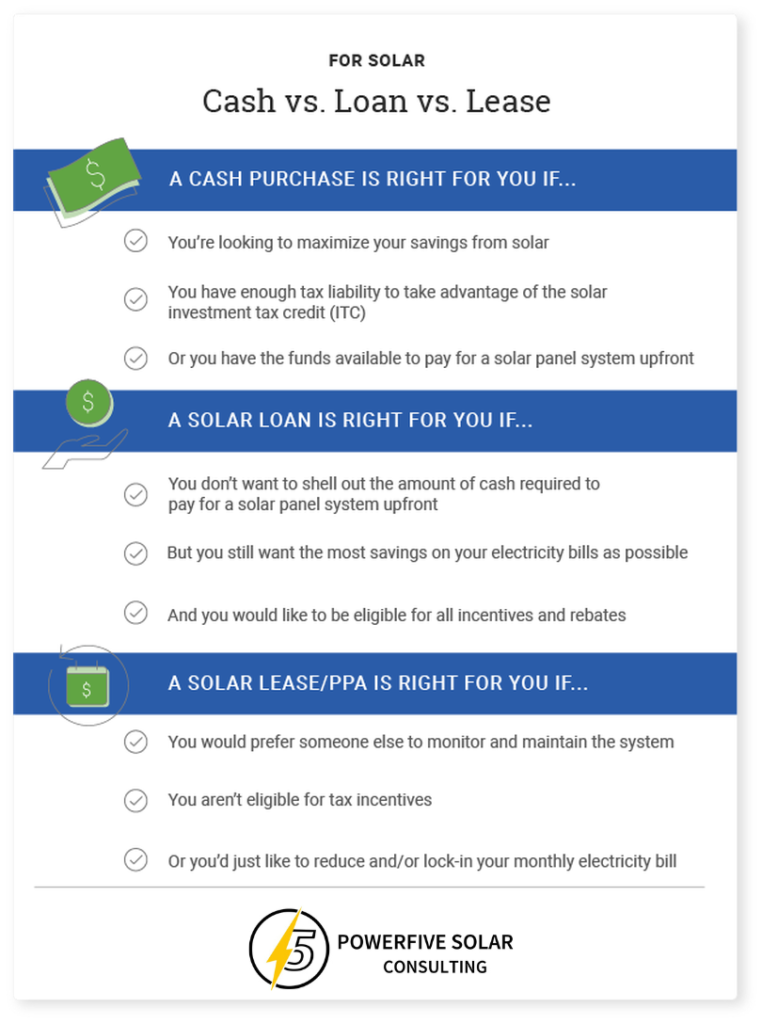

Cash vs. Loan vs. Lease comparison for solar

A cash purchase makes sense if:

You have the funds to pay for a solar panel system with cash upfront.

You want to maximize the financial benefits of going solar. A cash purchase will net you the highest return on investment (ROI) for your solar system.

You want to take advantage of the ITC and other tax incentives and rebates.

You want to own your solar system outright.

A solar loan makes sense if:

You don’t have enough funds to pay for your solar system with cash upfront.

You still want to maximize your savings as much as possible.

You want to take advantage of the ITC and other tax incentives and rebates.

You want to own your solar system outright.

A solar lease or PPA makes sense if:

You’re not looking for the highest return on investment (ROI) from your solar system.

You aren’t eligible for the ITC or other tax incentives.

You don’t care about owning your solar system outright at the end of of your lease or PPA.